Informing U.S. engagement with the world

The Latest in U.S.-China AI Competition

By Michael Froman

India’s Cockroach Party Protests Have a Powerful Precedent—and It Isn’t the Arab Spring

By Sadanand Dhume

Will Iran Turn Into a Forever War?

By Ray Takeyh

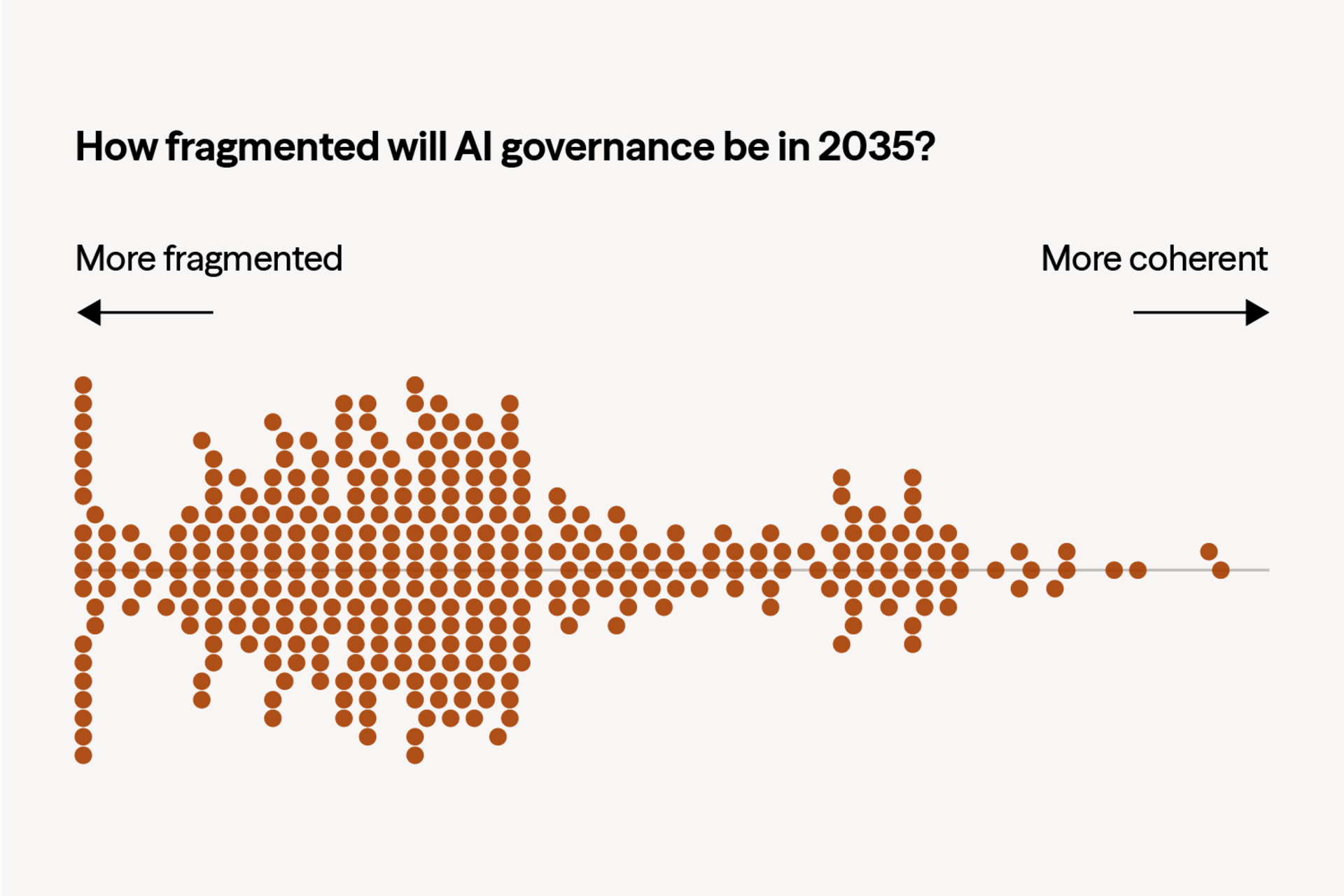

CFR Surveyed 350 Experts About AI’s Future. Here Are the Takeaways.

By Jessica Brandt and Adam Segal

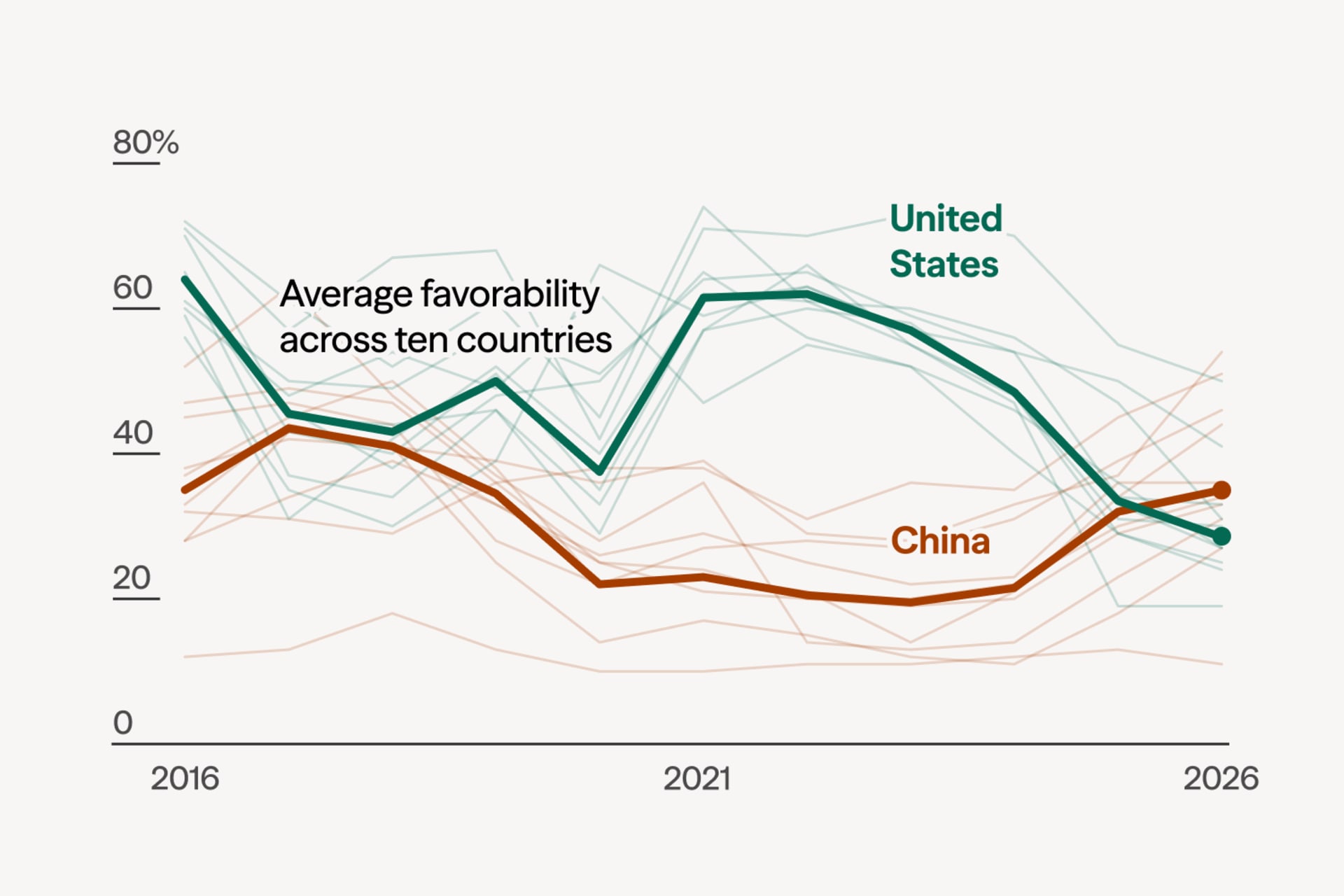

AI’s Economic Winners

By Rebecca Patterson

Iran War’s Ripple Effect

Expert Take

Expert Take Expert Take

Expert Take Expert Take

Expert Take Expert Take

Expert Take Expert Take

Expert TakeNavigating the AI Moment

Expert Take

Expert Take Expert Take

Expert Take Expert Take

Expert Take Expert Take

Expert Take Expert Take

Expert Take

Survey Results: How AI Will Change the Global Balance of Power

The rise of AI means policymakers need to navigate a future defined by technological uncertainty. To help them do so, CFR asked foreign policy experts to predict how frontier AI capabilities and the governance structures that could emerge around them will affect the global order.

Around the World

CFR analyses and explainers that address global issues and challenges.

The Saudi Nuclear Deal Would Set a Dangerous New Proliferation Precedent

By Erin D. Dumbacher

The U.S.-Saudi Nuclear Deal Set Off Tremors. Is It Still Alive?

By Steven A. Cook

Andy Burnham: What to Expect From the UK’s New Prime Minister

By Matthias Matthijs and Benjamin Harris

Trump’s New Tariffs: What to Know

By Michael Froman

The ICC Has Real Flaws. Dismantling It Without an Alternative Is Not the Answer.

By John B. Bellinger III

250 Years of American Foreign Policy

Expert Take

Expert Take Expert Take

Expert Take Expert Take

Expert TakeThe 10 Best and 10 Worst U.S. Foreign Policy Decisions

Council on Foreign Relations

Congress Checks Out

By Elliott Abrams

Where Does American Strategy Go From Here?

By Rebecca Lissner

The Coming AI Backlash

By Chris McGuire

Between Two Orders

By Charles A. Kupchan

After Hegemony

By Gideon Rose

Starting From Scratch

By Paul B. Stares

Overreach and Retrenchment

By Stephen Sestanovich

Podcasts

View AllThe Spillover

Every geopolitical event — a war, an election, a new tariff, a technological breakthrough — sends ripples through the global economy. On The Spillover, Sebastian Mallaby and Rebecca Patterson trace those ripples, examining how international developments shape markets, policy, finance, and the future of business.

1:02:21Podcast

1:02:21Podcast

51:39Podcast

51:39Podcast

Crisis Response Playbooks

The Wachenheim Center for Peace and Security has developed a set of Crisis Response Playbooks for U.S. policy planners when bandwidth is limited and decisions are consequential.

When armed conflict disrupts a critical maritime trade route, the United States can monitor, contain, or escalate the situation economically or militarily.

When a U.S. partner state faces a hybrid attack by an unknown aggressor, the United States should draw on various available response options to protect its treaty commitments, credibility, and commercial interests.

When a coup occurs abroad, the early hours of the crisis are most crucial for preserving and promoting U.S. interests—whether countering terrorism, checking adversaries‘ regional influence, upholding human rights norms, or maintaining diplomatic and economic relationships. Policy planners should therefore prepare for the unexpected.

Insurgency-related conflicts often start without warning and can last over a decade, making the pre-crisis and early crisis phases crucial for U.S. policymakers seeking to prevent national security threats and humanitarian disasters from emerging. Effective responses involve a complex set of legal authorities and international frameworks and require the sustained support of the American public and local communities.

CFR Events

View All

Publications

CFR publishes reports and papers for the interested public, the academic community, and foreign policy experts.

The Pharma Choke Point

Executive Summary U.S. dependence on China for essential medicines is structural—deeper, broader, and more consequential than conventional market analyses suggest. That dependence began with generic medicines and their ingredients but is now growing in biologics manufacturing, first-in-human trials, and synthetic DNA. That dependence is not simply the result of market conditions but rather decades of […]

Introduction Since the breakup of the Soviet Union, Russia has made a concerted effort to keep Belarus in its sphere of influence. Belarus’s political, economic, and military autonomy has ebbed and flowed over time, depending on geopolitical circumstances, Russia’s needs, and Belarusian President Alexander Lukashenko’s political adroitness. Nevertheless, the present moment poses unique challenges for […]

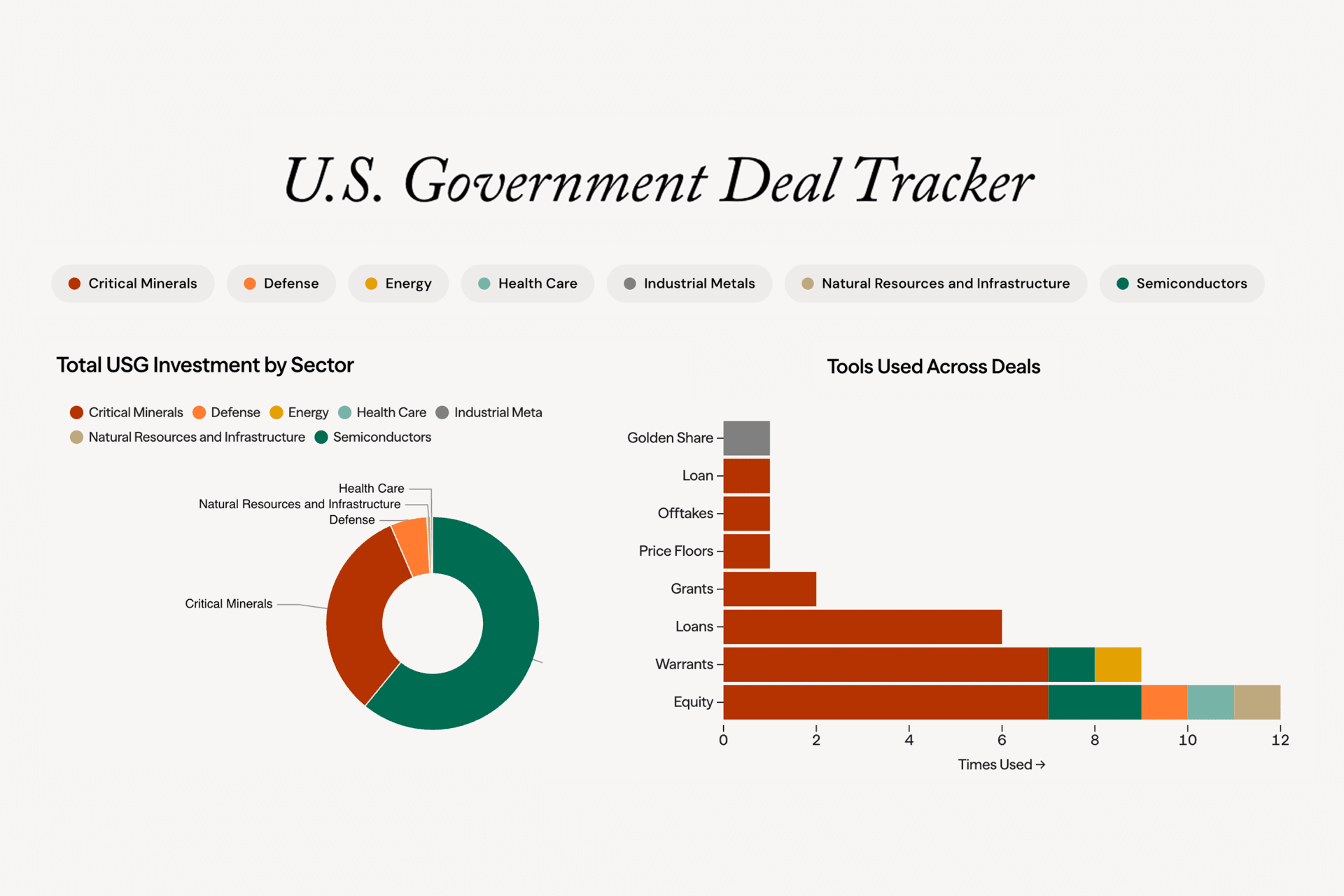

CFR’s U.S. Government Deal Tracker shows how the government is experimenting with new tools and financing structures to advance a range of strategic sectors, including critical minerals, energy, global logistics, manufacturing, telecommunications, and other technologies.

By Jonathan E. Hillman

A gap in private funding for companies and projects inhibits energy innovation in the United States. This “missing middle” slows or blocks technologies that could help the energy system become more secure, affordable, reliable, and sustainable from advancing through the demonstration and scale-up stages. Recent events have made the missing middle wider.

Suzanne Maloney, vice president and director of the Brookings Institution’s Foreign Policy Program, recommends that the United States reconsider its assumptions around eventual leadership change in Tehran, revive regime accountability efforts, prepare for opportunistic escalation by proxy groups, and ready itself for renewed nuclear diplomacy.

CFR International Affairs Fellow in National Security Roxanna Vigil argues that the United States should engage early with Colombia’s next administration to signal support for full implementation of the 2016 Peace Accords and provide targeted assistance.

The United States cannot out-mine and out-process China. Instead, it should leapfrog China’s dominance by scaling disruptive innovation, recovery, and recycling.

CFR in the News

View All

15 Books Longlisted for 2026 Cundill History Prize

Quill & Quire

The weaponisation of trade

Financial Times

When the dollar became a weapon

Blockworks Daily

Latest Content

View AllExpert Take Expert Take

Expert Take Expert Take

Expert Take