Online Store

Online Store

Sour on Europe

More on:

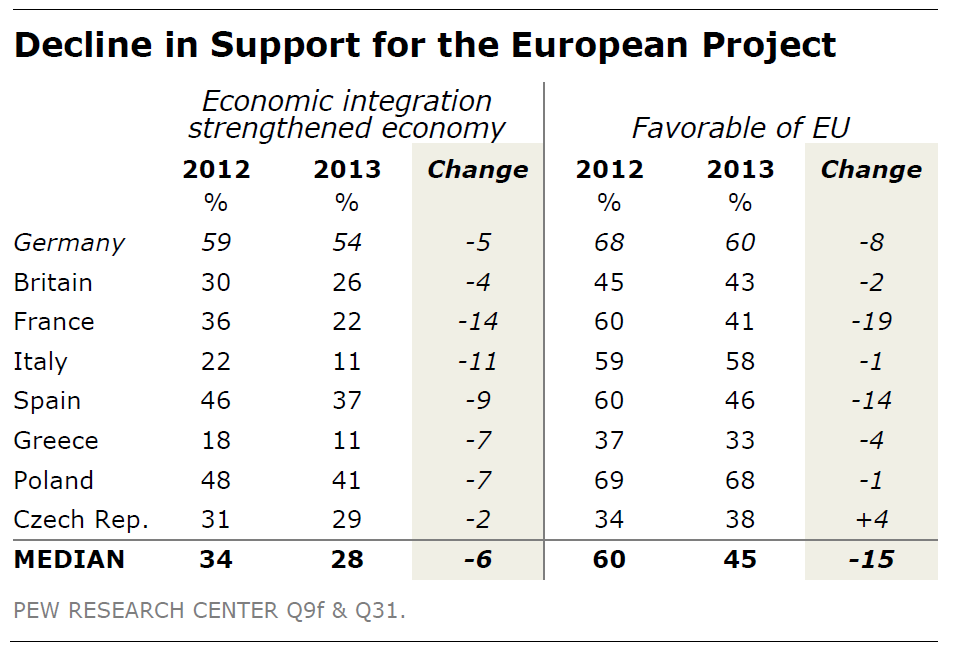

The most recent Pew Survey on European attitudes (summary table below) shows that support for the European integration project is dropping. My colleagues at CFR are far more able than I am to address the broader political ramifications of this shift. A few points though on the link between economic growth, public opinion, and support for the European reform agenda.

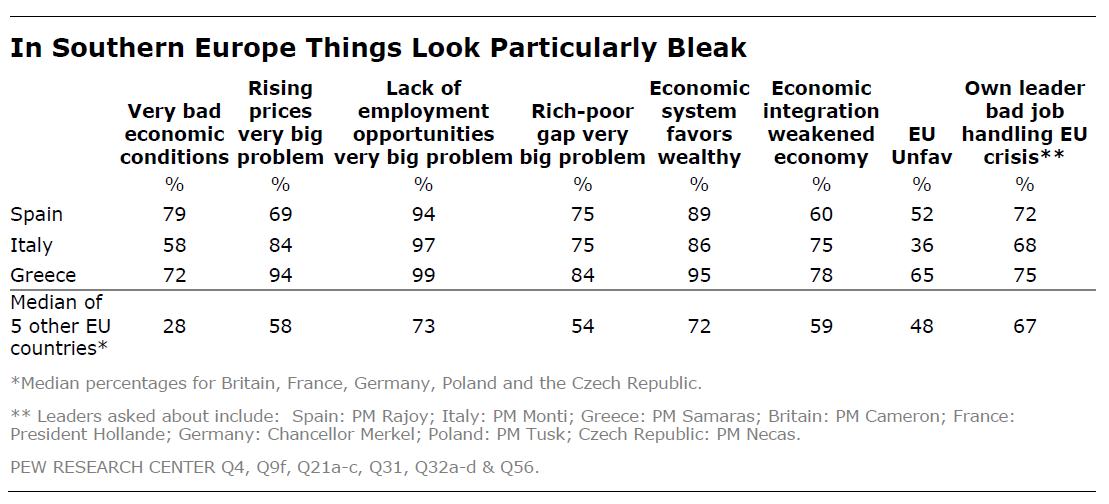

- Growth matters. Today’s Eurozone GDP numbers remind us that Europe remains in a grinding recession; a second-half recovery now looks to be a long shot at best. The only bright spot comes elsewhere, with news of a German labor deal that will raise engineering wages by nearly 6 percent over the next 20 months (rebalancing European demand and stimulating German consumption needs more of this). Some of the decline in the Pew numbers likely is cyclical, as declining confidence in their own economic prospects seems to spill over to other issues. Notably, the need for jobs dominates other issues on the economic agenda. The mood is particularly bleak in the periphery, reflecting those countries’ economic troubles. This is consistent with the idea the recession and diminishing expectations for the recovery are weighing materially on public opinion.

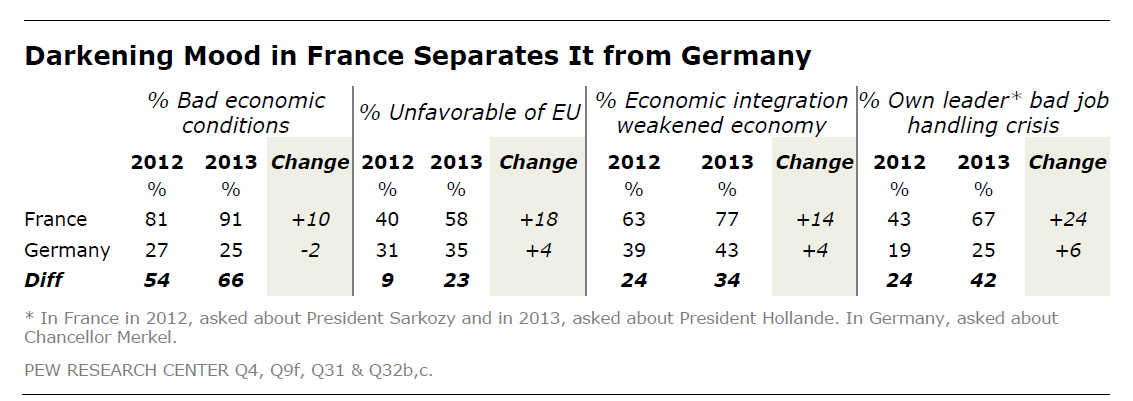

- A disillusioned France should matter to markets. The sharpest decline in sentiment in the survey--both for their own economic prospects and for the EU project--is in France. This coincides with other reporting suggesting declining confidence in the government’s ability to put the economy on the right track. In this regard, markets could be sensitive to a rise in opposition to the European project in France. The right-wing National Front (FN) party headed by Marine Le Pen has announced that it will run in next May’s EU parliamentary elections on a platform calling for an referendum on the euro. How would markets react if--fueled by disillusionment with the government’s economic program--the FN was the first past the post in those elections?

- Will a single chart damage Europe’s efforts to resolve the crisis? I missed this when it first came out, but it’s still worth a look. Last month, the ECB’s Eurosystem Household Finance and Consumption Survey presented estimates, for households, of median net wealth and the median value of their main residence. The interesting datapoint: Germany is at the bottom. Belgium, Spain and Italy (and, yes, Cyprus) all have household wealth several times German levels.

When this was released last month, the German press had a field day with the message that Germany shouldn’t bail out rich southern Europeans. There was pushback: it was noted that if means rather than medians were used, Germany would be in the middle of the pack (reflecting a more skewed German income distribution). Further, the high proportion of renting rather than buying homes in Germany means more housing wealth is off the household balance sheet. Broader measures of national wealth, including capital, restore Germany to the top ranks in terms of income.

The Pew survey (taken before the release of the chart), conversely shows Germans still support the European project, and are willing to pay to support it. (By 52 percent to 45 percent, Germans support bailouts for countries in crisis, compared to 40 percent in favor in France.) It remains to be seen, though, whether the chart below and the pessimism reflected in the Pew Survey resonates with less affluent German voters already suffering from bailout fatigue.

More on: